Can you live on $3,755?

Can You Actually Live on $3,775 a Month?

In my last post, “You want me to save $620 a month? How?”, I felt both your frustration and your relief. The math was simple, but it didn’t feel realistic.

That reaction is the point. Personal finance is not just math. It is behavior, tradeoffs, and constraints. It requires more than formulas. It requires honest conversations.

I left you with a question: Can you live on $3,775 per month?

Let me show you how I would approach that question if I were starting today. This framework is designed for someone early in their career. If you have dependents or more complex obligations, your numbers—and your decisions—will look different.

This is the constraint. Everything flows from here.

Financial Recap

Let’s ground this in a real example:

Gross Salary: $65,000

Annual Take-Home: $45,300

After deductions, 6% 401(k) contribution, and a 3% employer match

Monthly Take-Home: $3,775

From here, we apply a simple framework to make decisions:

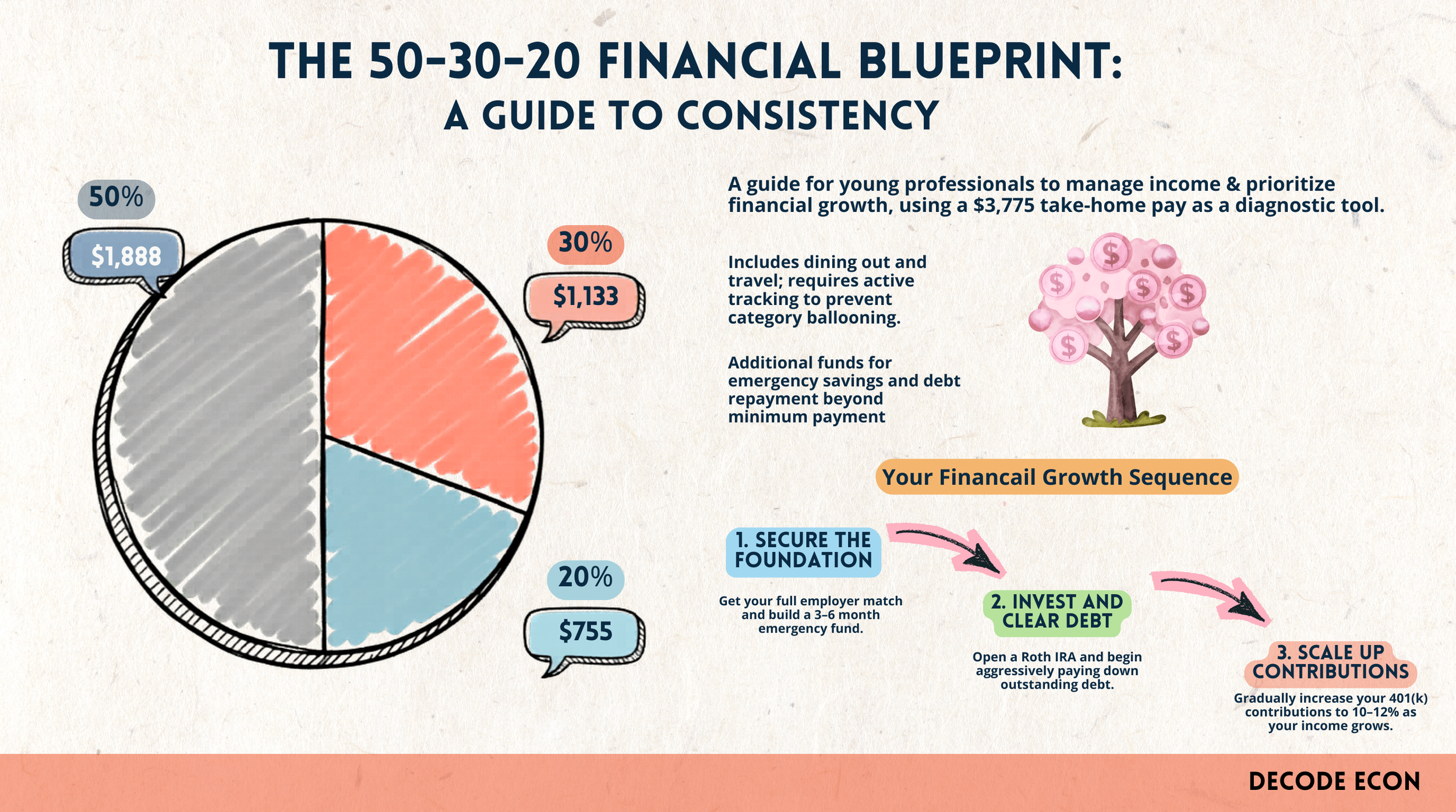

The 50–30–20 Rule

This is not a rule to follow blindly. It is a tool to help you see where your money is going—and whether your choices align with your priorities.

How the 50–30–20 Budget Actually Works

The 50–30–20 rule is not a law. It is a framework. It helps you see where your money is going and whether your spending matches your priorities.

50% Needs: $1,888 | 30% Wants: $1,133 | 20% Savings & Investing: $755

Needs

This is your baseline life:

- Rent

- Utilities

- Groceries

- Transportation

- Insurance

- Minimum debt payments

Be careful with insurance coverage. Just as you can be underinsured, you can also be overinsured.

Wants

This is where life happens:

- Dining out

- Travel

- Subscriptions

- Shopping

- Entertainment

The issue is not always overspending. More often, it is unplanned spending that slowly expands.

Savings & Investing

This category includes:

- Savings

- Investments

- Debt paydown

This is on top of the $487 already going into your 401(k) through employee and employer contributions.

The Hard Truth About Needs

Here’s the constraint most people do not want to hear: if your rent is too high, the entire system breaks down.

Housing is not just another line item. It affects everything else. Where you live matters, and for many people early in life, roommates may be necessary.

In my generation, having roommates was common. I get the sense that it is less common now, but it is still one of the most powerful financial decisions a young adult can make.

Roommates are not just a financial decision. They are also a life decision. They can expand your network, your social exposure, and your opportunities. In your 20s, that matters more than people realize.

In a city like Cincinnati, keeping rent around or below $1,200 is still a realistic target, even without roommates.

What the Budget Actually Looks Like

- Needs: $1,888

- Wants: $1,133

- Additional savings, investing, and debt paydown: $755

- Total monthly take-home allocated: $3,775

- Retirement savings already contributed to 401(k): $487

- Total savings and investment: $1,242

The Part Most Advice Ignores

The 50–30–20 rule is not a law. It is a diagnostic tool. I use it from time to time to make sure I am still aligned with my own goals.

As your income rises, be careful about where the extra money goes. When my income increased, I chose to direct more of it toward savings and investments.

More recently, rising grocery prices and travel costs forced me to revisit that allocation. That is normal. A budget is not something you set once and never touch again.

What This Framework Can Reveal

- If your needs are too high, you likely have a housing or fixed-cost problem.

- If your savings are not happening, your wants are probably untracked.

- If everything feels tight, your margin is too thin and every dollar already has a job.